Are your genes uninsurable?

Your genetics shouldn’t be a financial curse.

At least, that’s what Australia has decided.

The nation just banned life insurance companies from refusing to cover—or offering more expensive rates to—people based on their genetic testing results.

Why genetic testing interests life insurers:

- People often seek genetic tests to assess their risk of an inherited disease. For example, you might test for the BRCA gene to weigh breast cancer risk and consider prophylactic options like preventive mastectomy.

- Life insurers are in the business of weighing your risk of dying—based on your age, sex, race, and other information. A genetic test revealing you’re more likely to be ill or die earlier is a gold mine for their risk assessment.

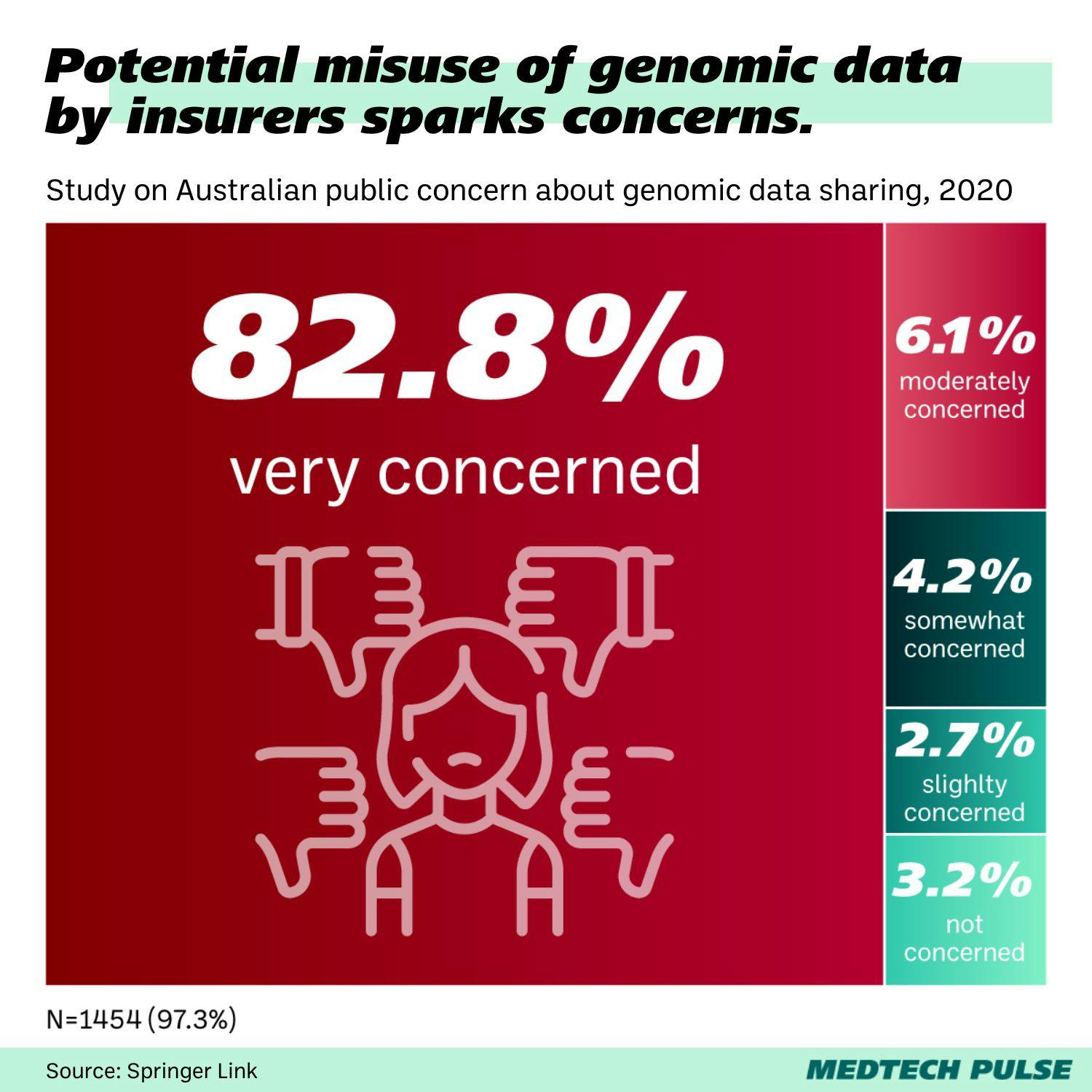

Why does this matter?

Families of people denied life insurance or other coverage bear greater financial strain, creating more inequities for the chronically ill. Plus, the risk of being denied coverage keeps people who may greatly benefit from information about their genetic risk (e.g., people with a family history of cancer) from getting tested.

That’s why this is often referred to as genetic discrimination.

How do other countries police genetic discrimination?

- Canada: in 2017, adopted the Genetic Non-Discrimination Act.

- U.K.: since 2001, has an agreement between the insurance industry and the government that prohibits genetic testing from being factored into underwriting.

- U.S.: banned the use of genetic results in health insurance underwriting in 2008, but life insurance is still fair game, with certain states considering policies on this topic (i.e., Florida).

- Many countries in Asia and Europe also have explicit bans against genetic testing being used for insurance purposes (e.g., Austria, Ireland, Singapore).

Still, many other countries don’t have explicit policies dictating what insurance can or cannot do if it gets ahold of your genetic information. And others have policies like the U.S., which bans health insurers from doing genetic discrimination, but not life insurance.

These shifting regulations are a big reason why we must continue to emphasize information security and clear communication in the medtech space. Patients and users need to understand what is being done with their health information—even if they may not understand the stakes upfront.

Take 23andMe’s history. Over just a few years, the purpose of DTC genetic testing went from being for finding lost relatives to being for fun to being for health—to a mix of all three.

Companies pivot. We find new applications for medical innovations. Through it all, we must keep patient safety and well-being at the forefront. And if the information we help patients discover about their bodies may lead to harms in other areas of their lives, that’s our concern, too.

In the meantime, I’m happy about the Australian government’s decision to protect its residents. May the rest of the world follow in their example.